What is a Money Mule?

A money mule is a person who conducts fraudulent transactions from their bank account to another person, or who allows someone else to take full control of their bank account.

The table below explains the difference between a money mule and an operator.

| Money mule | Money mule operator |

| Adding to the definition above, it is a person who receives money from a third party into their bank account, transfers it to another person, or withdraws it in cash and gives it to someone else, in exchange for a commission. | A person responsible for selecting money mule victims and organizing their work process. |

Money mule operations are a part of the expanding chain of money laundering by criminals, including drug traffickers and organized crime. Fraud scams that use mule accounts target the vulnerable who knowingly or unknowingly transfer illicit profits. These scams may also link your organization to organized crime financing, which is a serious Anti-Money Laundering (AML) offense.

The cumulative losses from money laundering are estimated at around $1.6 trillion, or 2.7 percent of global GDP. Group-IB’s 2025 Digital Risks Highlights report estimates total annual damage from Classiscams at $120 million to $720 million.

This highly organized scheme involves fake online marketplaces and classified ads designed to steal a victim’s financial details. The stolen funds are often funneled through networks of money mule accounts or cryptocurrency wallets to evade detection.

Money mule victims are “groomed” by scammers and become enablers of criminal activities before they know it. The underlying intent is to make it harder to trace the origins of criminal funds. While the entire process is carried out to mimic a legitimate business activity, there are red flags to watch out for.

To avoid being lured into acting as a mule, be skeptical of unsolicited job or “easy cash” offers. This includes impersonation scams, in which criminals pose as trusted individuals or organizations to deceive victims. Scenarios can involve “bank fraud teams” advising victims to transfer their funds to a “safe” account or revealing valuable details that can be abused to access bank accounts.

How the Money Mules Network Works

Money mule scams use recruited or stolen accounts to move illicit funds. Fraudsters disguise these transactions as legitimate activities to build trust and avoid detection before activating the network for money laundering.

But what gives scammers an understanding of how much time they have for money withdrawal? Let’s look at the most commonly used money mule approach.

1. Account Creation

The organizer convinces the money mule to create an account or provide his own at the first step. New accounts are often made on financial service applications that require a minimum of documents. People for this step can be selected from the unemployed or from those with low income who are not concerned about the risks of participating in fraudulent schemes.

2. Warm-Up

This stage is often called “warming up” the account among criminals. To do this, small payments are made to increase the account’s trust level and reduce the likelihood of later detection of larger transfers. The warm-up phase can be challenging to detect with conventional AML filters, particularly when combined with recycled “clean” accounts.

3. Account Takeover and Money Transfer

During an account takeover, fraudsters seize the victim’s account or the entire network, depending on the nature of the attack.

4. Money Withdrawal

The final step involves withdrawing funds from ATMs or transferring them to cryptocurrency through exchange services. The latter approach is more popular because the operator can do it independently, having all the necessary data about mule accounts.

Is Cryptocurrency the Most Prevalent Means of Exploitation?

Cryptocurrency has a history of being exploited for money mule operations because of its speed, pseudo-anonymity, and cross-border reach. Fraudsters often use small- and medium-sized crypto exchanges to move or withdraw stolen funds through highly liquid cryptocurrencies like Tether or privacy coins like Monero.

In most countries, cryptocurrency isn’t a genuine payment instrument. Many small and mid-size exchanges still lack mature KYC (Know Your Customer) processes and real-time screening controls, creating blind spots for Anti-Money Laundering (AML) teams. This means they are less equipped to provide reliable information about clients making suspicious transactions. This setup allows operators to independently control funds once they leave a mule’s bank account, significantly complicating the money trail.

Criminals’ appetite for cryptocurrency cashouts extends beyond classic mule rings. In Group-IB’s investigation on crypto drainers, scammers posed as tax authorities to trick victims into fake duty payment sites. The money was then funneled through small exchanges with weak KYC, mirroring the blind spots that money mule operators exploit. We expect mule operators to keep abusing these loopholes until worldwide FATF Travel-Rule alignment and full MiCA supervision take hold.

It is essential for cryptocurrency exchanges to undergo a security audit. This assessment evaluates all aspects of your environment, including the blockchain network, website, application, and smart contracts for potential risks.

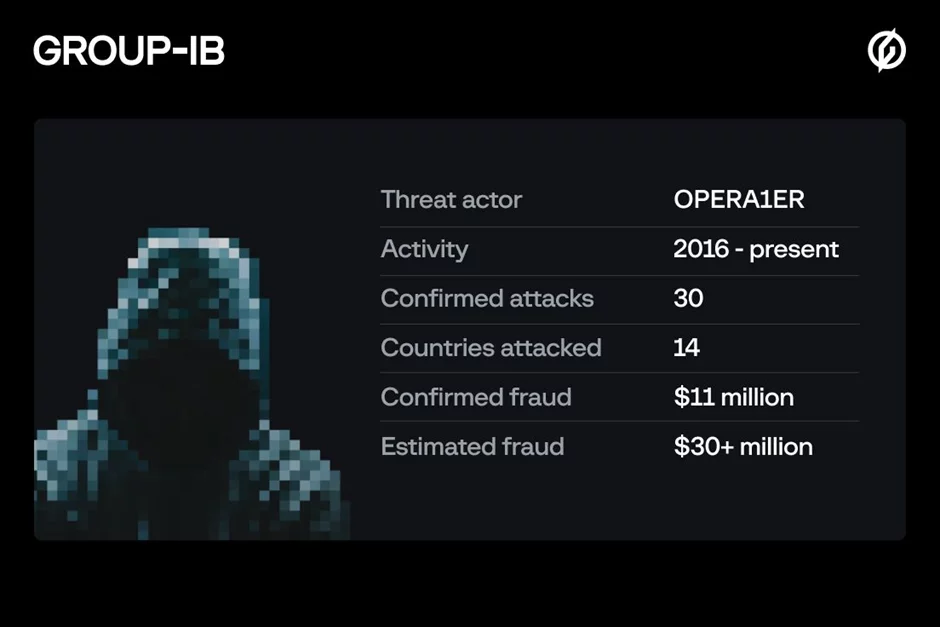

OPERA1ER’s Money Mule Scam

Group-IB uncovered money mule scams by the infamous threat actor, OPERA1ER, who repeatedly attacked banks to execute fraudulent transactions and seized millions. Our leading team of cybersecurity experts tracked the most frequent victims, their geographies, the vulnerabilities they used, and the maneuvers they employed over the years.

The final phase of the attack often occurred on weekends, when OPERA1ER would exploit the banking infrastructure to fraudulently transfer funds from customers’ accounts to mule accounts. Mules, hired by OPERA1ER, would conduct “cash out” exercises, withdrawing money from numerous ATMs.

Read how we uncovered the threat actor’s malicious activities in the full report, “OPERA1ER: Playing God Without Permission”.

Strategies to Detect and Block Money Mule Activity

Organizations can detect and block money mule activity by incorporating non-transactional intelligence (such as device fingerprinting, session behaviour anomalies, and account relationship analysis) into their AML prevention procedures.

Below are key non-transactional indicators your AML team can use to detect and block mule activities at every stage, from account creation and takeover attempts to fund transfers.

Indicators During Account Creation

During the account creation, if the money mule account and the victim are in the same bank, then the money mule account preparation can be detected by the following non-transactional indicators:

- Access from one device to multiple simple bank accounts

- The intersection between devices and user accounts that aren’t related to work, family, or other relationships

- Use of virtual phone numbers or throw-away email domains during registration

- Consistent mismatches between ID documents and the device’s IP geolocation or system time zone

Indicators During Account Takeover and Money Transfer

These non-transactional indicators can help prevent illicit activity during the account takeover and money transfer stages:

- Access to the legitimate user account of a new device that the user did not previously use

- Access through the general or high-risk VPN services

- Access from a known scam device

- Checking payment details with a list of compromised or money mule accounts

Advanced behavioral and technical analysis can further strengthen your defenses by identifying suspicious mule activity, such as multiple accounts on the same device, network, or application, the use of anonymization tools, activity from restricted or high-risk locations, and non-unique installation dates.

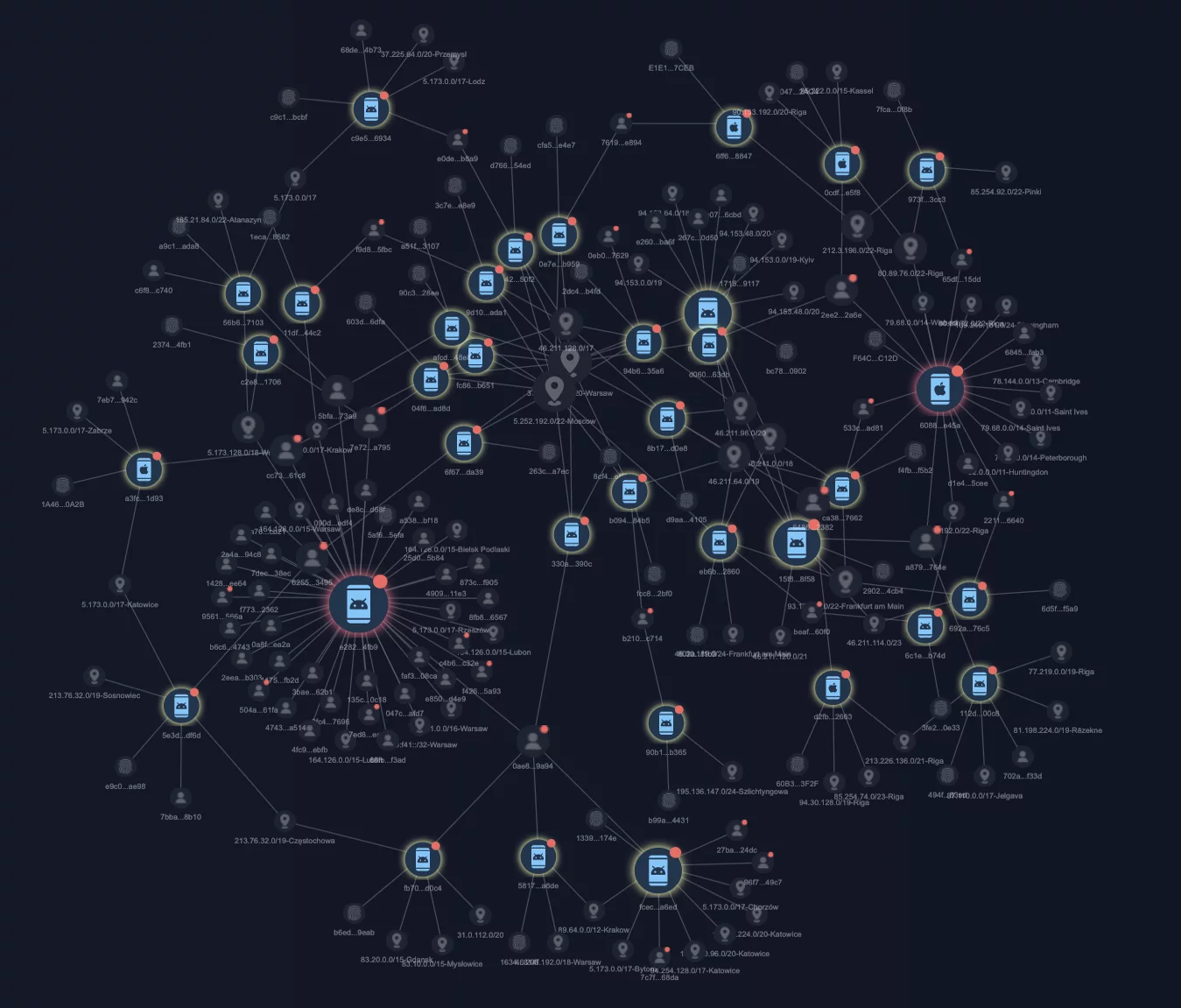

The visual below shows an organized money mule network with over 70 user accounts and 30 devices.

Figure 1 – The graph enables you to see all the information (devices, customers, and IP addresses) attached to 70 accounts flagged as mule accounts.

Here is Group-IB Fraud Protection’s graphical representation of a device connected to multiple bank accounts.

Figure 2 – Dive deeper into the investigation with a detailed overview of each device and its associated transaction record.

For further mitigation strategies, our blog, “Strengthening AML Defenses: Detect Money Mules During Their ‘Warm-Up’ Phase” explores both transactional and non-transactional indicators to ensure that no threats slip through.

How Group-IB Protects Your Organization From Money Mule

Early mule detection and identification allow organizations to proactively block or restrict accounts before they are used for money laundering. Group-IB Fraud Protection leverages advanced user session telemetry monitoring and network analysis to expose money mule accounts, even during their setup and warm-up phases.

Here’s how our anti-fraud solution adds a critical layer to your AML defenses:

- Advanced technical and behavioral profiling detects mule accounts through device fingerprinting, unusual device usage, and anomalous activity patterns.

- Relationship analysis uncovers complex mule networks by linking accounts with devices or global IDs associated with known mule activity

- Real-time risk scoring and alerts on suspicious accounts for timely investigation and intervention

- Integrated threat intelligence for maintaining updated blocklists of known mule-associated devices, synthetic identities, and recruitment URLs.

Watch this explainer video to understand how Group-IB’s advanced fraud protection technologies work in real-time. Or get in touch today for a demo on our early mule detection and identification system to protect your customers from money mule operations.

Fraud Protection

Tailored specifically for industries, learn how Fraud Protection offers unbeaten detection and protection against modern attacks.

If you or your organization have been a victim of a money mule scam, you can contact the local authorities to seek immediate assistance.

FAQs About Money Mules

1. What is the difference between a money mule and a scam victim?

A money mule is a person who transfers money obtained illegally to criminals, whereas a scam victim is someone whose money was stolen in the first place.

2. Are money mules always aware they are committing a crime?

Money mules can include those who are unaware that they are committing a crime. Victims are lured by deceptive tactics (such as fake job offers or online romances) and believe they are involved in legitimate activities.

3. What industries are most affected by money mule operations?

Money mule operations affect industries that process fast, remote payments, such as banks, money-transfer services, e-commerce marketplaces, travel booking sites, and cryptocurrency exchanges.

4. What technologies help detect mule activity in real time?

Fraud detection technology that leverages behavioral analysis, device fingerprinting, and machine learning algorithms can help you detect money mule activity in real time.