Identifying Compromised Cards

This is the second article in a two-part series on compromised card intelligence for non-issuing entities. Part 1 examined why e-commerce and iGaming have been structurally excluded from accessing compromised card data, and how Distributed Tokenization changes that equation. This article is written for fraud operations and risk teams who need to understand the mechanics: what happens inside the matching process, what the response payload contains, and how it integrates into an existing transaction authorization workflow.

Key Takeaways

- Traditional pre-authorization checks miss a critical fraud signal: device, behavioral, and network analytics can flag suspicious sessions, but they do not reveal whether the card itself is already compromised

- Distributed Tokenization transforms card data inside the participant’s own environment and exchanges only irreversible tokens, making compromised card checks usable before authorization

- Group-IB’s Cyber Fraud Intelligence Platform provides a privacy-preserving threat intelligence layer that helps reduce downstream fraud losses without requiring raw data exchange

The Gap in Your Pre-Authorization Stack

Most fraud teams already have a layered pre-authorization stack. They assess device reputation, behavioral anomalies, transaction velocity, IP geolocation, and proxy or VPN use to determine whether a payment session looks suspicious. These controls are valuable; they excel at evaluating the environment around the transaction. What they cannot evaluate is the card’s compromised status.

That gap matters more than it may appear. A transaction can look completely legitimate at the session level: the customer may be returning, the device may be familiar, the behavior may fall within expected patterns, and the network signals may raise no immediate concern. Yet the card being presented could already be circulating in a dataset harvested from stealer malware, dark web marketplaces, or underground forums.

In that scenario, your fraud stack sees a clean session, while the actual payment credential is already exposed. The issuer may not yet have flagged the card. The average delay between a card breach and customer awareness ranges from 14 to 30 days. The chargeback arrives weeks later, by which point the transaction is settled and goods or services have been delivered.

This is the blind spot in many pre-authorization workflows. Existing controls answer questions like ‘Does this session look unusual?’ or ‘Does this user’s behavior deviate from baseline?’ What they do not answer is the more direct fraud question: ‘Is this card already known to be compromised?’

For organizations in e-commerce and iGaming, the commercial impact compounds quickly. A single compromised-card transaction can exceed the face value of the purchase when you factor in chargeback losses, dispute-handling costs, exposure to scheme penalties, and increased pressure on chargeback thresholds.

What has been missing from pre-authorization fraud checks is not another behavioral flag or device signal. It is threat intelligence: a real-time way to determine whether the card itself has already appeared in known compromise datasets.

Group-IB’s Threat Intelligence unit brings that missing layer into the fraud workflow through a repository of more than 200 million compromised payment card records, built from continuous monitoring of dark web marketplaces, stealer malware botnets, and underground forums. The Cyber Fraud Intelligence Platform makes this repository queryable by non-issuing entities while ensuring that no party has access to the raw card data itself.

In practice, this gives fraud operations teams access to a signal they have historically lacked: whether the card number presented in a transaction is linked to known compromise activity. And it does so in a form that can be consumed before authorization.

Distributed Tokenization: How It Works

Distributed Tokenization is a multi-stage cryptographic process that transforms sensitive data such as a Primary Account Number into an irreversible, pseudonymized token. That token can be matched against other tokenized datasets, but it cannot be reversed to recover the original card number.

This is the mechanism at the center of the architecture that makes compromised card intelligence usable without exposing raw payment card data.

Unlike conventional tokenization models that may send sensitive data to a central service for transformation, Distributed Tokenization begins within the participant’s environment. The raw card number is processed locally, at the point where the organization already handles it as part of the transaction flow. Only the transformed output leaves that environment.

The Core Challenge

An organization needs to check a card number against a repository of compromised card records, but neither the organization nor the platform should exchange raw card data during that lookup. A useful fraud signal cannot come at the cost of expanding the attack surface.

The Cyber Fraud Intelligence Platform addresses this through Distributed Tokenization, a patented process that converts sensitive identifiers into irreversible pseudonymized tokens. The system preserves matchability for threat intelligence purposes while removing the need to expose the original underlying identifier.

Where the Transformation Happens

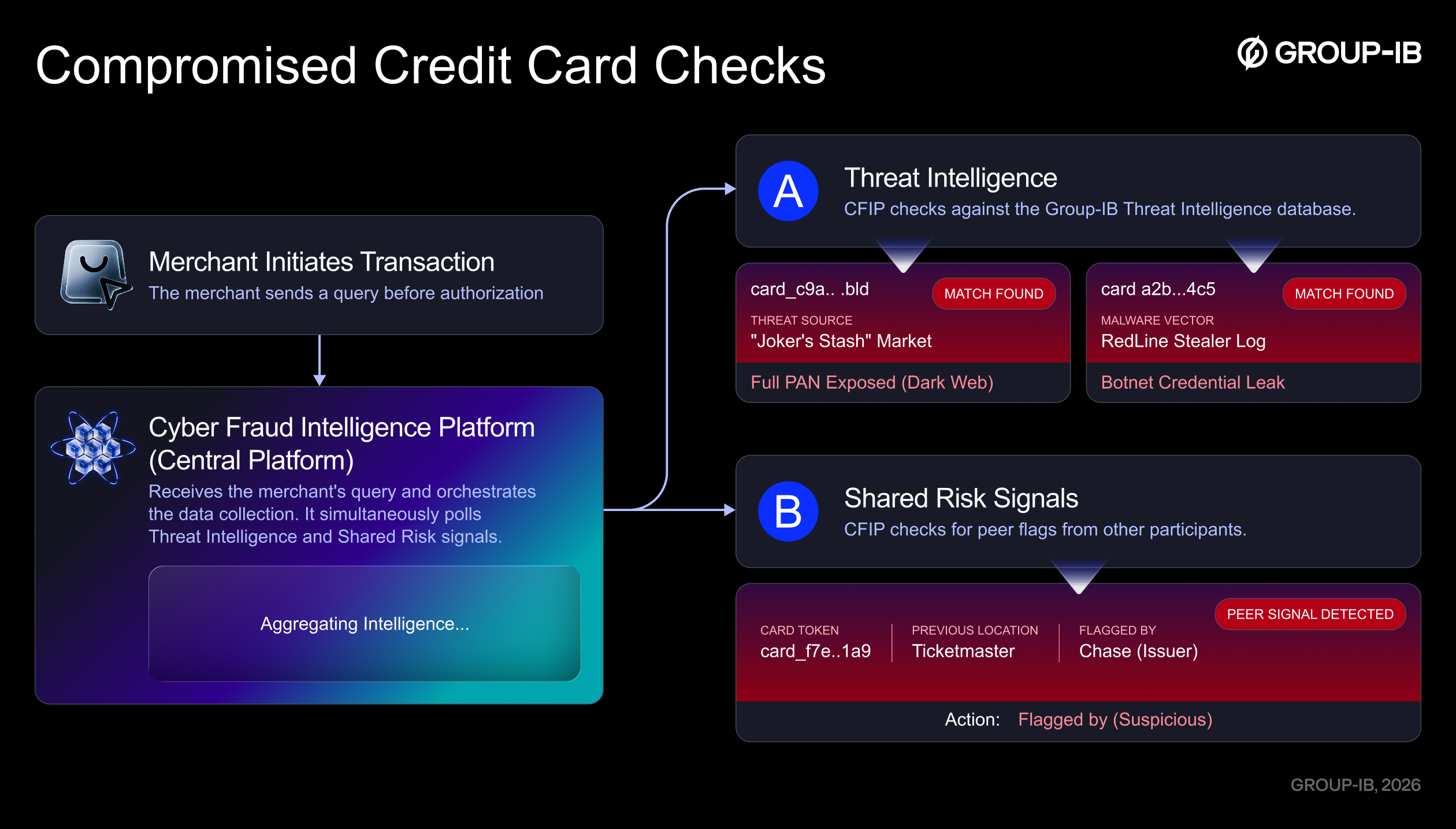

The first step occurs within the participant’s environment via the Cyber Fraud Intelligence Platform Connector. This component acts as the outbound gateway between the organization’s transaction processing system and the wider network.

When a payment card is presented, the Connector receives the raw card number locally and performs the initial cryptographic transformation there, before anything is transmitted externally. The raw card number never leaves the participant’s perimeter. What leaves instead is only the transformed output; the tokenized form.

This point is crucial for both architecture and compliance. The lookup begins with sensitive data where it already exists legitimately, and from that point forward, the system operates on a privacy-preserving representation rather than the live card number.

The cryptographic design has been independently assessed by Bureau Veritas Cybersecurity, which validated both its resilience and its compliance with GDPR data protection principles.

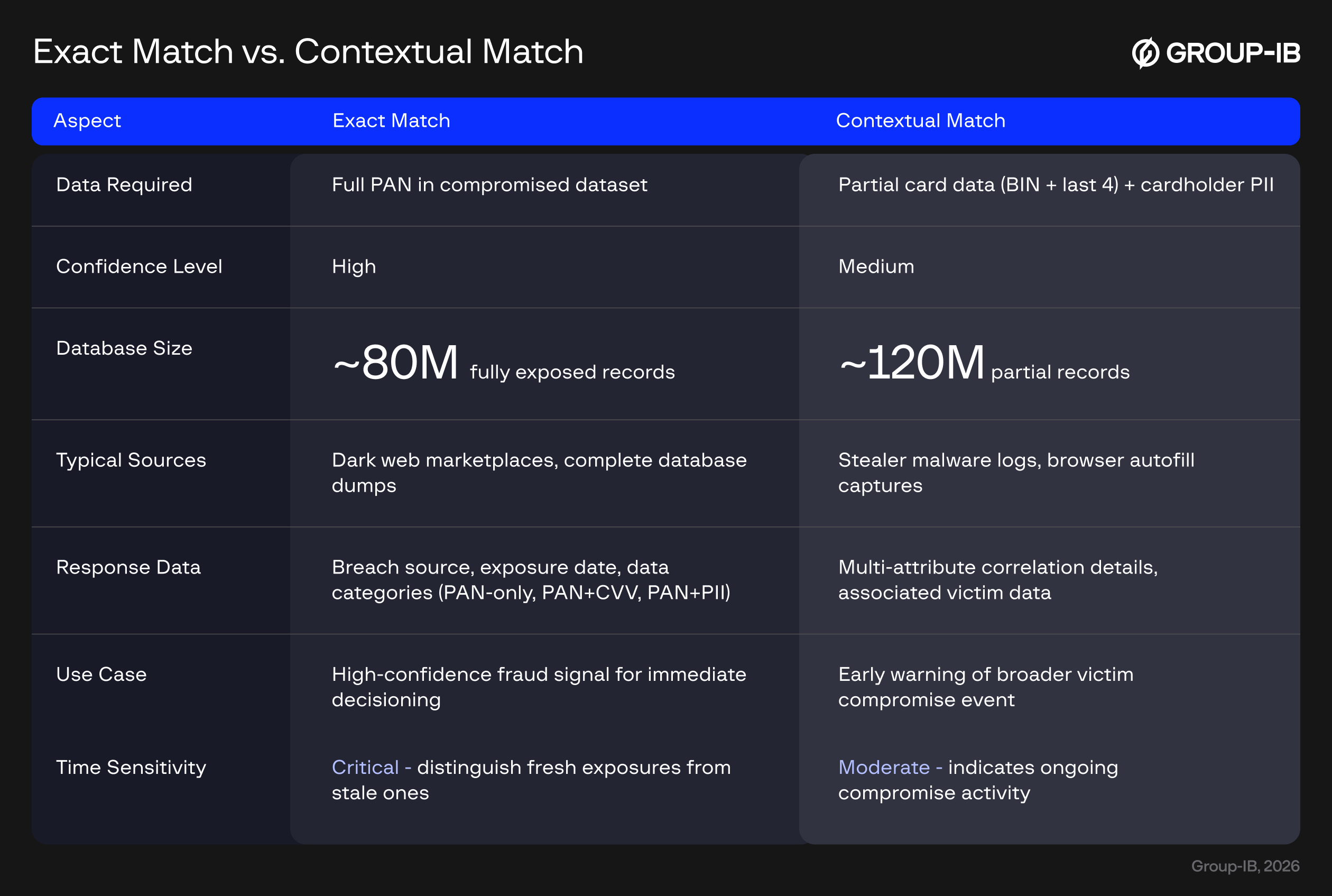

Two Matching Modes: Exact and Contextual

The response a fraud team receives depends on how strongly the presented card data aligns with known compromised records. The platform expresses that alignment through two matching modes: Exact Match and Contextual Match.

Together, they allow the platform to surface risk across both fully exposed card records and partial-compromise data which is especially important in modern fraud investigations, where threat data is often incomplete, fragmented, or captured in different forms.

Exact Match

An Exact Match occurs when the tokenized card number corresponds directly to one of the approximately 80 million fully exposed card records in Group-IB’s repository. These are cases where the complete card number was recovered from sources such as dark web marketplaces or stealer malware logs.

Because the full card number is represented in the compromised dataset, the resulting signal is the strongest and most operationally actionable. For a fraud team, the value of an exact match extends beyond knowing that the card is compromised. The response also provides surrounding threat context: where the card was first observed, when it was exposed, and what level of data was exposed alongside it, whether that means card-only, card-plus-CVV, or card-plus-cardholder information.

That additional detail matters because it can affect how a fraud engine responds. A card found in an older marketplace dump doesn’t necessarily carry the same immediate risk as a card that appeared in a stealer malware log within the last 48 hours. In the first case, issuers may already have received reactive alerts through mechanisms like CAMS or SAFE, and the card may already be under monitoring or replacement. In the second, the compromise may still be fresh, active, and not yet fully visible to the issuer.

This makes an exact match more than a binary fraud flag; it’s a time-sensitive threat signal that helps organizations distinguish between stale exposure and active criminal use.

Contextual Match

A Contextual Match applies when the compromised dataset does not contain the full card number but includes partial card data, typically the first six and last four digits alongside related personal information such as the cardholder’s name, email address, or physical address. In these cases, the platform performs a multi-attribute correlation rather than a direct one-to-one card number match.

This is where the matching model becomes especially relevant to real-world fraud operations. Many modern compromise sources, particularly stealer malware logs, do not always yield a clean, fully exposed payment card record. Instead, they may capture fragments: saved autofill details, browser-stored credentials, partial card numbers, contact details, cookies, and other victim-linked artifacts.

On their own, those fragments may not be enough to prove that a specific card number is compromised. But when several tokenized attributes align within the transaction context, they can still form a meaningful intelligence signal.

For example, if the first six and last four digits from a transaction align with a compromised record, and the cardholder name or email also aligns with the same victim data captured in a stealer log, the system can return a contextual match even though the full card number was never present in the original dataset.

This makes the signal lower confidence than an exact match, but far from noise. It tells the fraud team that the transaction materially overlaps with known compromise evidence and warrants attention. In many cases, it serves as an early warning that a payment attempt is part of a broader victim-compromise event.

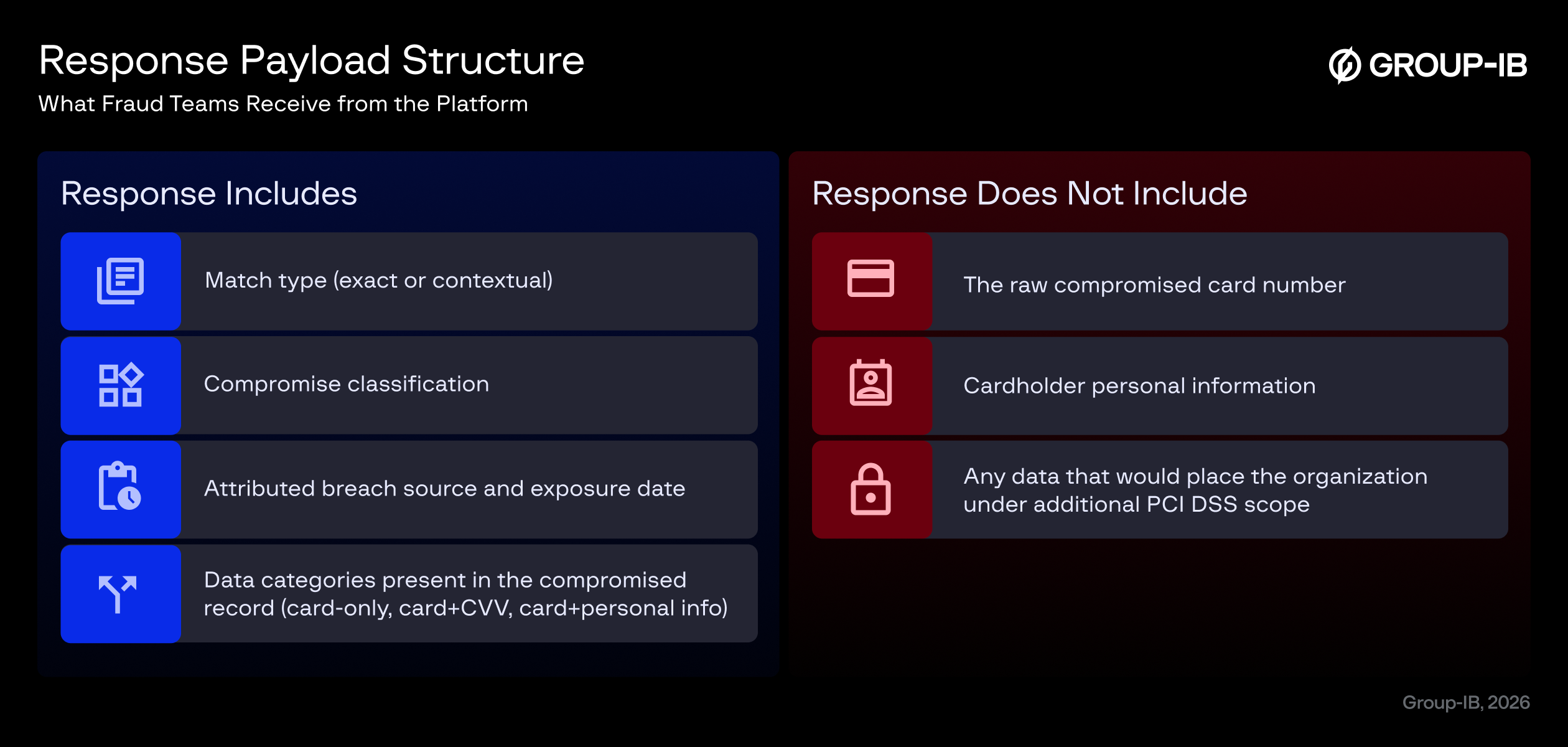

What Appears in Your Fraud Queue

For fraud operations teams evaluating integration, the platform response is designed to serve as structured threat intelligence input rather than a raw data feed. It includes the core fields needed for decisioning, while explicitly excluding any data that would expose cardholder information.

The response includes:

- Match type (exact or contextual)

- Compromise classification

- Attributed breach source and exposure date

- Data categories present in the compromised record (card-only, card-plus-CVV, card-plus-personal-info)

What it does not include:

- The raw compromised card number

- Cardholder personal information

This is a decisive point for integration architecture. The response functions as threat intelligence input, comparable in form to a reputation lookup or an external watchlist check, rather than as a data feed that requires its own storage, encryption, and access controls. The Connector handles the cryptographic operations locally; the organization’s fraud platform consumes a structured intelligence response and determines its own course of action.

Integration With Existing Transaction Flows

The Cyber Fraud Intelligence Platform provides intelligence, not verdicts. The platform returns a structured risk signal; it does not score transactions, make authorization decisions, or recommend actions. How that signal is consumed is entirely at the discretion of the querying entity’s fraud operations team.

That said, the intelligence is designed to be consumable at pre-authorization, meaning the card check can occur after the customer submits payment details but before the transaction is authorized and settled. This positions the compromised card signal alongside existing pre-authorization risk inputs, where the organization’s own fraud engine determines how to act on it.

How a fraud team chooses to use the signal will depend on their risk appetite and operational model. An exact match with a recent exposure date carries different implications than a contextual match on older data. Some teams may treat a confirmed compromise as grounds for immediate decline; others may feed it into an aggregate risk score alongside device, behavioral, and network signals. The decision architecture remains with the organization. The platform supplies the intelligence layer that was previously unavailable.

The network dimension adds a second layer. Because the platform operates as a collaborative system, a card that generates a chargeback or is flagged as suspicious by one participating entity whether a bank, an acquirer, or another organization produces a peer-to-peer risk signal visible to all other participants. This converts isolated fraud events into shared network intelligence without exposing the underlying card data between participants.

Independent Validation of Distributed Tokenization

The Distributed Tokenization mechanism itself has been independently assessed by Bureau Veritas Cybersecurity. That assessment evaluated both the cryptographic design of the tokenization process and its alignment with GDPR principles, including pseudonymization, data minimization, and data protection by design.

This matters because privacy-preserving architecture claims carry more weight when they are externally reviewed rather than asserted solely in product messaging. Bureau Veritas’s assessment concluded that Group-IB’s approach aligns with GDPR principles as of September 2025, providing compliance and legal stakeholders with an additional assurance layer beyond payment-card controls alone.

One Layer in a Broader Defense Strategy

Group-IB supports this approach by integrating Digital Risk Protection for brand monitoring and takedown, Threat Intelligence for infrastructure analysis and dark web tracking, Fraud Protection for behavioral detection, and Investigation services for attribution. For fraud operations teams, this means the ability to detect compromised card campaigns at their source, correlate signals across multiple fraud vectors, and act before losses occur rather than reacting after chargebacks arrive.

The Cyber Fraud Intelligence Platform represents one mechanism within this model: it provides cross-institutional intelligence sharing for organizations that need it. But the coordinated approach works equally well when fraud teams integrate external threat intelligence with their internal controls without requiring data-sharing networks. The principle is integration rather than isolation, making fraud prevention capabilities work together instead of operating as disconnected tools.

The compromised card intelligence described here addresses one specific gap in pre-authorization fraud detection. But modern fraud operations increasingly require coordination across multiple detection layers and intelligence sources, an approach the industry is beginning to refer to as Cyber Fraud Fusion. Rather than operating fraud prevention systems in isolation, it integrates external threat intelligence (such as dark web monitoring and malware analysis) with internal fraud controls (session analysis, behavioral detection, transaction monitoring) and coordinated investigation workflows.

For organizations building mature fraud programs, this means connecting threat intelligence that tracks compromised credentials and emerging fraud tactics with real-time fraud decisioning systems, then routing confirmed cases to investigation teams for resolution.

What This Means for Your Fraud Program

For fraud teams, the value is straightforward: card compromise intelligence adds a signal that most pre-authorization stacks still lack. Device, behavioral, and network checks can show whether a session looks suspicious, but they do not answer the more direct question: Is the card itself already known to be compromised?

That makes this signal fundamentally different from existing fraud inputs. A transaction can appear normal at the session level but still involve a card exposed in a marketplace dump or stealer malware log. By bringing that intelligence into pre-authorization, Group-IB helps fraud teams detect risk before a transaction settles and later returns as a chargeback.

For organizations in e-commerce and iGaming, the business case is clear. A compromised-card transaction can lead not only to direct loss, but also to chargeback fees, dispute handling costs, and growing pressure on chargeback thresholds. Earlier visibility into exposed cards helps reduce those downstream costs and strengthens decision-making at the point where action is still possible.

What makes this especially relevant is that the intelligence layer now exists without requiring raw data exchange. With Distributed Tokenization and privacy-preserving matching, adding compromised card checks to pre-authorization workflows doesn’t mean moving raw account data outside the customer environment.

The gap in fraud decisioning has been clear for years. The difference now is that there’s a practical way to close it. The question is no longer whether this intelligence is useful, but whether fraud teams can afford to keep operating without it.

Fraud teams already know how to assess suspicious sessions. Group-IB helps them assess compromised cards before the loss is realized.

Want to see how Group-IB can add compromised card intelligence to your pre-authorization stack? Talk to our team about how the Cyber Fraud Intelligence Platform supports earlier fraud detection with a privacy-preserving, compliance-conscious architecture.